7/14/2025

Last week was perhaps the first sign that the summer holidays are on the way. Just the one deal priced, and it seems a fair few bankers might already have one eye on their villas in the French Riviera and the September pipeline.

Indeed, it should be no surprise just as schoolchildren enter the ‘watch a film vaguely related to a lesson and be quiet’ stage of the school calendar.

Those kids will also be getting their end of year report cards dissected over dinner with the parents. The phrase “D for disappointing” still rings in my mind when I look back on my education. (Relax, I got A*’s in the end).

So, with all that in mind, I thought now would be the perfect time to take stock, and give European ABS its own H1 Report Card.

But first, to the lonely deal of the week, BNP Paribas PF’s French Consumer ABS, the €1.15bn Noria 2025 FCT.

It is the second deal from the Noria series, after Autonoria Spain 2025 was priced in June.

This time around, the €925.7m AAAs were retained and offered in equal measure, coming in about 8bps to finish at 57bps over 1-month Euribor. There was yet again strong coverage from investors, with the offered €462.5m books ending 2.8x covered.

Meanwhile, further down the stack coverage was incredibly strong at 5.4x, 7.8x, 6.7x and 7.1x for Classes B-E. No surprise then, that with no competition that spreads came in aggressively as a result.

In terms of issuance, it’s been a slightly odd year so far. There has been a tendency to feel dissatisfied with the pace of play. Perhaps with demand so strong, investors so clearly desperate for more, many thought there would be an extra incentive to come to market.

Yet, comparatively, it has still been a very strong first six months, despite a very serious wobble in the middle.

Placed issuance finished at €68.7bn, just €200m shy of the H124 figure, and of course, 2024 ended up being a record year for issuance post-GFC of €130bn.

It’s amazing how quickly one can forget, and perhaps 2023 can serve as a useful reminder, that over €50bn of paper in six months hasn’t been the norm for very long at all.

The question going forward of course will be whether the momentum can be sustained as it was last year. There is more tariff talk coming, but it remains unclear what will happen. Similarly, wars in Ukraine and the Middle-East have the potential to drastically alter market perceptions.

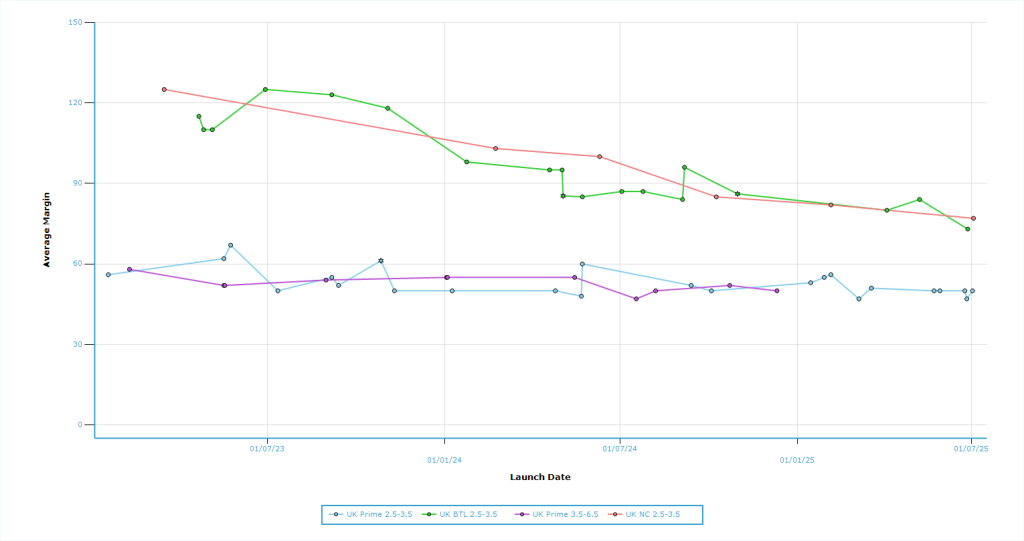

As for spreads, well, it’s just kept getting tighter and tighter – particularly in the UK.

Figure 2 (below) shows AAA spreads for UK RMBS in Non-Conforming (2.5 WAL), Buy-to-Let (2.5-3.5 WAL), and Prime (2.5-3.5 WAL and 3.5-6.5 WAL).

For both Non-Conforming and BTL, spreads have reached some of their tightest levels since the war in Ukraine began. In some cases, the pickup between BTL and Prime could be as low as 20bps, in from over 50bps at the beginning of 2023.

Prime paper seems to have a floor at around 47bps over Sonia, as we’ve seen for the last few years. But what’s been impressive is how the smaller names like debut issuer Newcastle Building Society, have been able to print at the same levels as the biggest high-street lenders.

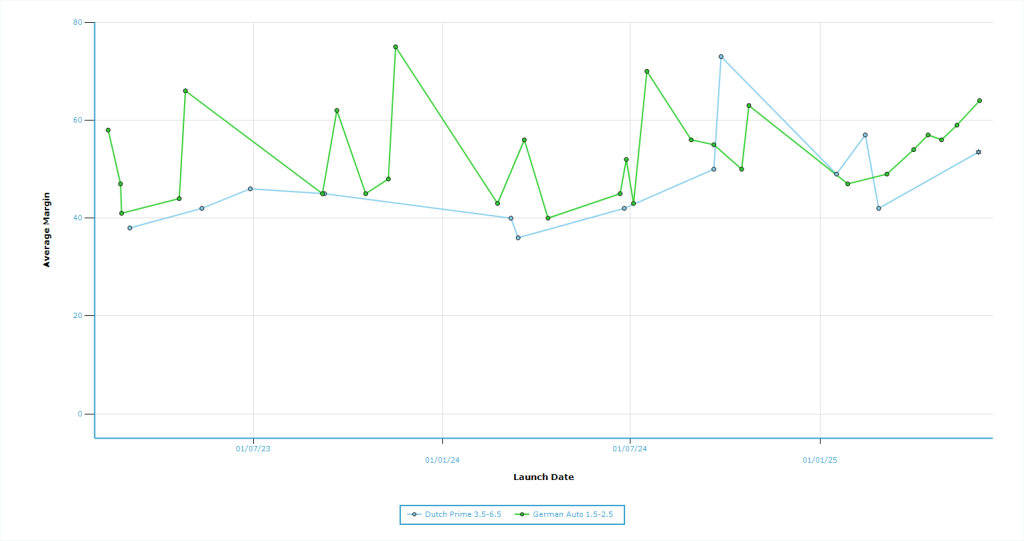

The picture is less clear when it comes to Euros, however. Stalwarts of the market like German Autos and Dutch Prime haven’t been able to make much progress, with AAA spreads generally drifting a tad wider over the course of the year. But they are still oscillating around that normal range for this type of paper, without any ECB liquidity programs of course, as Figure 3 (below) shows.

Meanwhile, Consumer ABS has done well and after the success of Noria last week, now looks to be honing in on some of the tightest levels seen in over 2 years.

All in, it’s a positive return for the market. Let’s hope September gets off to a strong start, and maybe topping €130bn is in sight after all.

All this talk of school reminded me of my days using playing in a band as a way to escape lessons. The practice rooms were hidden under the school stairs to make it a natural studio, and so no non-music teacher knew it even existed! Unfortunately, I had no talent to play any musical instrument very well, so I had to end up singing.

However, the deal was that we did actually have to perform at some point.

And 16 years on from the last time we performed at school, my band – Lemmon and the Pips – took the stage once more, as we prepare for our performance at the Guitarist’s mother’s 70th birthday this week.

Below is our warm-up gig on Saturday and me in an Elvis suit back in 2010…

Have a great week!

Tom

© 2026 ARC Risk Models Limited