8/26/2025

Click here to sign up to the mailing list

“I want you to put the word out there that we back up.”

No, I’m not referencing Stringer Bell (Idris Elba)’s famous line in The Wire to talk once more about my beloved Arsenal and their 5-0 win this weekend and £67.5m purchase of Ebere Eze. Of course, the real story this week is that European ABS has risen from its summer slumber and we have live deals already in the pipeline – before the bank holiday!

In addition, this Monday saw Volkswagen’s VCL, the bellwether prime Auto ABS, return to action as well.

Not one, not two, but THREE deals hit screens last week. Bank11, through its longstanding RevoCar platform, kicked things off on Monday with a German Auto ABS. Then, on Tuesday, SocGen launched its own Auto deal with Red & Black France.

You would be forgiven for thinking that as euro deals are naturally less affected with a UK bank holiday on August 25th, it’s just a case of more bankers and investors on the continent being back to work. Right? Wrong

On Wednesday, Charter Court kicked off the sterling market by launching CMF 2025-1, its third Prime RMBS in as many years.

So here we are, at least a week earlier than expected, European ABS is back up.

And Arsenal have brought Eberiche Eze home.

All three deals are marketing into this week, with all expected to price by the end of Friday, 29th of August.

Bank11’s RevoCar 2025-2 is provisionally sized at €400m, with the AAA-rated Class A tranche taking on the lion’s share at €371.2m. There are three sub-€10m pieces offered below that.

This edition would make it the third year in a row that Bank11 have come to market twice, marking the bank as a truly established force in Auto ABS – their first deal came way back in 2014.

Hot on their heels came SocGen with a similarly well-regarded brand in Red & Black. This is the first time French collateral has appeared in 2025 though, after Red & Black Auto Germany 12 priced back in May.

Red & Black Auto Loans France 2025 is the full name, backed by a 1-year revolving €650m provisional portfolio of auto loans. However, final sizing is still TBC at the point of publishing.

There’s only one tranche on offer, the AAA-rated Class A’s, which will represent 88.5% of the total deal size.

That’s the deal information, but I suppose the real question is why now? Of course, it’s not unusual for issuers to hit screens in late August – even before the UK bank holiday. And you could also argue that it’s becoming increasingly common.

It’s also not the case that Red & Black’s announcement is a reaction to Bank11’s, as SocGen is the arranger for both deals.

It does however suggest that bankers are expecting a hectic September, and that their main fear over the coming month or two is probably investor “indigestion” rather than something like market volatility drastically changing spreads on offer.

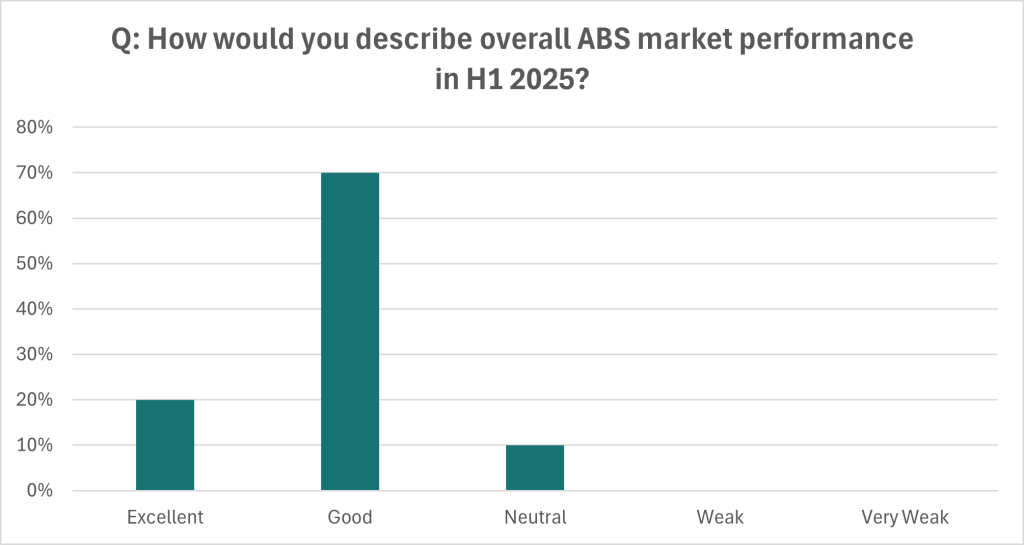

In preparation for this week being yet another quiet one, I had myself armed with the results to the Freshly Squeezed Summer Survey we began a month ago. (Thank you for the great responses, by the way).

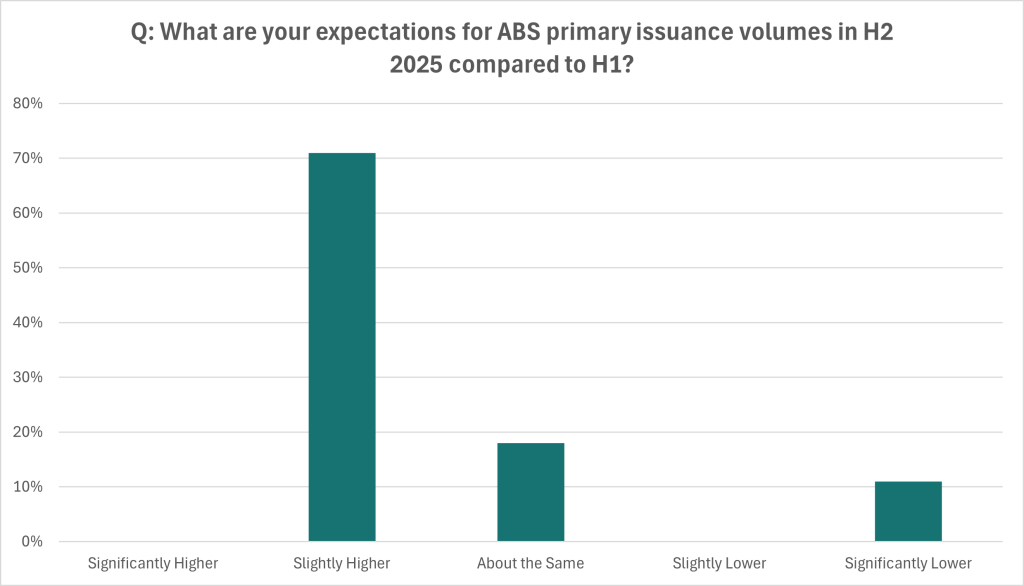

But it remains useful here. 71% of respondents said that they expect ABS primary issuance to be “slightly higher” in H2 2025 than H1. Over 40% also said that investors were likely to be “slightly more optimistic” in the coming months too, with another 37% thinking they’d be about the same. In fairness, spreads can’t be much tighter can they!?

So, it appears that SocGen and Bank11 are being prudent. Investors can’t be full if these trades are already on your desk when you get back from the Algarve.

Our survey didn’t discriminate between euros and sterling, and so it is likely that the same thought process took place for Charter Court and its Prime UK RMBS CMF 2025-1. As with Red & Black, the deal size remains TBC, but there is a provisional pool of £592.2m. 91.25% will go to the Class A’s, however, a “portion” of that tranche will be retained by Charter Court.

Bank of America is the arranger here (and they are joint lead manager with SocGen on RevoCar), meaning again that CMF would have been well aware of the other fare coming through this week. Deutsche Bank and RBC join them as joint leads.

After a stop-start few years in Charter Court’s early RMBS career, which began in 2017, this is now their third consecutive year in the market. Pricing is targeted for the back end of this week, either Thursday or Friday.

That’s all from me this week. I leave you with an update that I spent this weekend battling my way into the Semi-Finals of the Sudbury Golf Club Matchplay Knockout, after a 3&2 victory over a 19 handicap.

Nerves nearly got the better of me when he showed Phil Mickelson-esque touch around the greens in the opening holes, but with my Dad holding bag, I ground him down in the end.

September 14th is my date to make it to Sudbury’s “Finals Day”. I am sure you will all wait with baited breath for the outcome…

Have a great week

Tom

© 2026 ARC Risk Models Limited