10/13/2025

Click here to sign up to the mailing list

One of the biggest challenges for the arrangers working in European securitization is known as “execution risk”. By that, they mean the time you are left exposed to vagaries of the financial markets while your deal goes through its auction process.

In most bond markets, bankers will have an early morning meeting where they make a call on whether to “go”, where they hit screens or “no go”, where they wait another day.

If they choose to go at say 8am, you can expect it to be all done by late afternoon that day. In securitization though, one could “go” on Monday morning and at best be done by Wednesday afternoon. More likely Thursday or Friday of that week.

That extra time, compared to say covered bonds, means securitizations inherently have greater execution risk.

I can recall, for example, a couple of deals getting caught out in the LDI crisis. I knew things were bad when no one was picking up my call. But one investor did eventually call back, and said something along the lines of, “how can I bid for an RMBS when gilts are starting the day up 50bps and then veering down below 100bps by the afternoon?”.

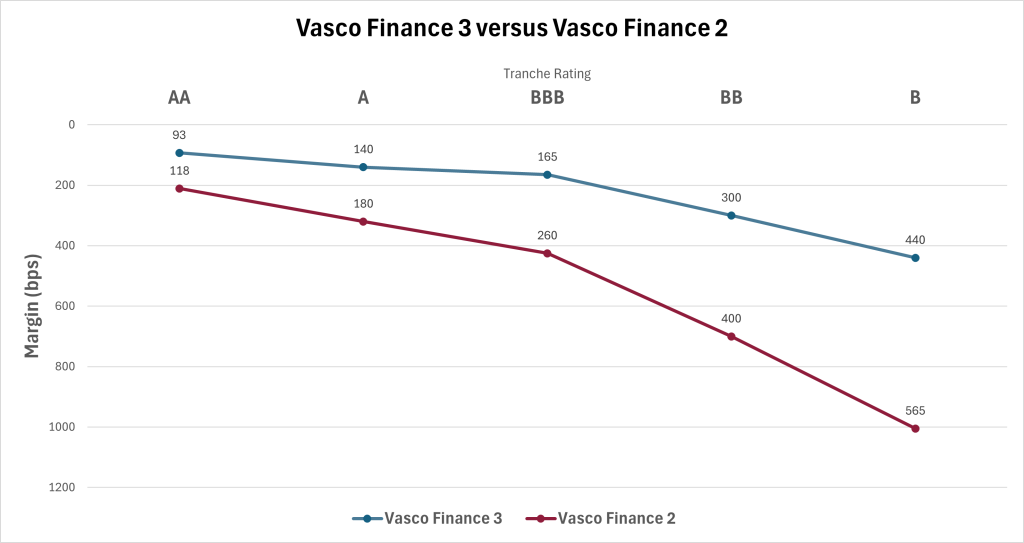

Something similar happened to Wizink bank last September, although the market volatility wasn’t anywhere near as extreme. The Portuguese lender’s credit card ABS hit screens with investors gobbling up anything they could get their paws on, but by the time they got to Wizink’s Vasco Finance 2, that exuberance had faded and Wizink had to pay up.

This time around though, the €300m Vasco Finance 3 was able to build solid momentum and priced tight of its IPTs after two rounds of guidance. Wizink hasn’t really changed anything from its last edition, but with slightly better luck, they’ve managed to come out with a much better result.

What a difference a year makes. Look at the graph below to see just how much.

Aside from Wizink’s rare European Credit Card ABS, the week in euros has been pretty strong for what is now mid-October. Six deals were priced this week, with just one of those pre-placed. However, none of the six came from the UK.

A word really should go to Santander, who have continued to be a tremendous presence in ABS this year. The bank hasn’t always pulled its weight considering the strength of its high-street presence throughout Europe, but the last few years have seen its securitization team go from strength to strength.

Yet again, they were in the market this week with two Consumer ABS deals, one being the Italian €505m Golden Bar 2025-2, and the second coming from Portugal via the €419m Consumer Totta 3.

In the Concept ABS league tables, with 32 deals across €7.2bn, Santander are third on deal count only to Bank of America (42 deals) and BNP Paribas (55 deals). However, both of those banks are also huge players in CLOs, while Santander are not.

The strength of Santander’s platform is really starting to show now. Investors back the brand, and deals from Italy and Portugal are not the risk they once were. With the now standard practice of cautious IPTs leading to runaway demand, even if there isn’t quite the same level of exuberance as early September, both deals got away well.

If this week was all euros, next week looks to be stronger for sterling (for once!).

Eight deals are in the pipeline, but there are five sterling trades, including the return of LendInvest’s buy-to-let shelf, Mortimer, for the first time since Halloween 2024. There’s also a £308m Prime RMBS debut coming from Shariah compliant home financier, StrideUp Homes, which is great to see.

In euros, the three deals include a Dutch debut from Beequip, an equipment leasing company with a full-capital stack on offer and another Prime Dutch RMBS from Oldenburgische Landesbank, who having taken their debut plunge with Weser Funding 2025-1 in February, are back at it once more just under eight months later.

That’s all from us this week. But before I go, just wanted to give a little bit of ARC news. ARC Ratings has hired Andrew Steel, formerly of Fitch Ratings, to be Global Head of Corporate Finance and Chief Analytical Development Officer. You can read more in the release here.

Finally, for those concerned readers wanting to know how I’m holding up, fresh from my pain of losing the golf final last week, I played at a nice little course in Amersham called Harewood Downs to help get the misery out of my system.

I could think of nothing I would less like to do than play golf again, but it was good for me.

And true to form, my second shot of the day was an awkward 9-iron which I hit within a foot of the flag. Not one came out like that on the prior weekend.

But in the words of the great orator (perhaps not golfer) Boris Johnson, them’s the breaks.

Have a great week

Tom

© 2026 ARC Risk Models Limited